To Ensure True and Fair Financial Reporting

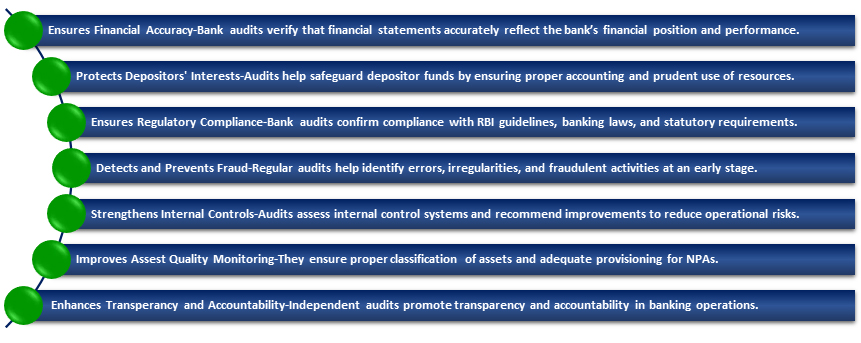

To confirm that the bank’s financial statements accurately reflect its financial position and performance

To Ensure Compliance with Banking Regulations

To verify adherence to RBI guidelines, banking laws, and statutory requirements.

To Verify Loans and Advances

To examine loan documentation, asset classification, and provisioning for credit risk.

To Safeguard Depositors’ Funds

To ensure depositor money is properly accounted for and protected against misuse.

To Assess Internal Control Systems

To evaluate the effectiveness of internal controls and operational procedures.

To Detect and Prevent Errors and Fraud

To identify material errors, irregularities, and potential fraudulent activities.

To Ensure Proper Income Recognition

To confirm that interest and other income are recognized as per regulatory norms.

To Evaluate Investments and Treasury Operations

To verify valuation, classification, and compliance of investment and treasury activities.

To Support Regulatory Oversight

To provide reliable audit findings that assist regulators in supervising banks.

To Enhance Transparency and Accountability

To promote clear, accurate reporting and responsible financial management.

To Strengthen Risk Management

To assess and improve the bank’s handling of credit, market, and operational risks.

To Build Stakeholder Confidence

To enhance trust among depositors, investors, regulators, and the public.