When is GST Registration Required?

- Year-end financial reporting

- Bank funding or loan requirements

- Internal control and management review

- Periodic verification for large inventory-based businesses

Get Quote Here

WHAT IS GOODS AND SERVICES TAX (GST)?

Goods and Services Tax (GST) is a comprehensive indirect tax system implemented in India on 1 July 2017 with the objective of creating a unified and transparent taxation framework. GST is levied on the supply of goods and services and has replaced multiple indirect taxes previously imposed by the Central and State Governments, such as Value Added Tax (VAT), Service Tax, Central Excise Duty, Entertainment Tax, and several others. By subsuming these taxes, GST has simplified the indirect tax structure and reduced the overall tax burden on businesses and consumers.

GST is a destination-based tax, which means that tax revenue is collected by the state where goods or services are consumed rather than where they are produced. This principle ensures fair distribution of tax revenue among states and removes barriers to inter-state trade. Under GST, tax is charged at every stage of the supply chain; however, the system allows businesses to claim Input Tax Credit (ITC) for the GST paid on purchases. This mechanism eliminates the cascading effect of tax-on-tax and ensures that tax is ultimately borne only by the final consumer.

One of the most significant features of GST is its dual structure, which allows both the Central and State Governments to levy tax simultaneously. In case of intra-state supplies, GST is divided into Central GST (CGST) and State GST (SGST). For inter-state supplies and imports, Integrated GST (IGST) is levied by the Central Government and later apportioned between the Centre and the States. In Union Territories without a legislature, Union Territory GST (UTGST) is applicable. This structure ensures seamless tax collection and credit flow across the country.

GST has introduced a technology-driven compliance system.Registration, return filing, payment of tax, and refund processes are carried out online through the GST portal. This digital approach has increased transparency, reduced manual intervention, and improved compliance. Businesses are required to maintain proper records, issue GST-compliant invoices, and file periodic returns, thereby bringing more accountability into the tax system.

Overall, GST represents a major reform in India’s taxation system. It has streamlined indirect taxes, promoted ease of doing business, encouraged formalization of the economy, and created a common national market. While the transition to GST initially posed challenges for businesses, continuous improvements and policy refinements have strengthened the system. Today, GST stands as a cornerstone of India’s economic and fiscal framework, contributing to long-term growth and transparency.

KEY BENEFITS OF GST

• Eliminates the cascading effect of taxes by allowing Input Tax Credit (ITC)

• Simplifies compliance by replacing multiple taxes with a single system

• Brings transparency through an online registration and return filing process

• Facilitates smooth inter-state trade and commerce

• Reduces overall tax burden and improves pricing efficiency

OBJECTIVES OF GST

• To create “One Nation, One Tax”

• To simplify indirect tax laws and procedures

• To widen the tax base and improve compliance

• To remove barriers to inter-state trade

• To increase revenue through better tax administration

IMPORTANCE OF GST

• Integrates India into a single national market

• Encourages formalization of businesses

• Improves transparency and accountability in taxation

• Helps reduce tax evasion

• Benefits consumers through competitive pricing and reduced hidden taxes

SCOPE OF WORK UNDER GST

• GST registration, amendment, and cancellation

• Determination of taxability and applicable GST rates

• Issuance of tax invoices and record maintenance

• Filing of monthly, quarterly, and annual GST returns

• Input Tax Credit (ITC) reconciliation and claims

• GST audit, assessment, and advisory services

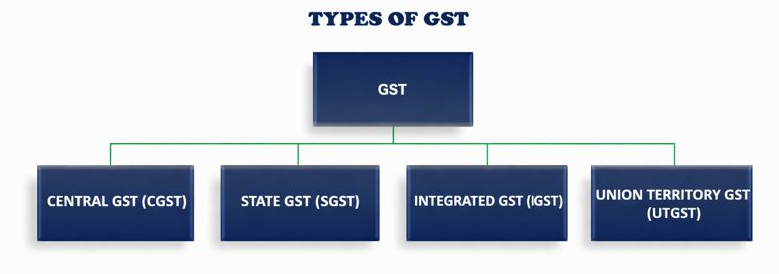

TYPES OF GST

SGST (State GST) is an indirect tax levied by the state government on intrastate (within the same state) supplies of goods and services. It is levied by the state government where the product is sold or consumed. SGST ensures that the state government gets its tax revenue share from intrastate transactions. SGST has replaced earlier state-level taxes like purchase tax, luxury tax, VAT, and more.

CGST (Central GST) is imposed by the central government on intrastate (within the same state) supplies of goods and services. An equal value of CGST and SGST is levied on the same intrastate supply. If GST of 18% is levied for an interstate transaction, 9% will be the CGST rate, and 9% will be the SGST rate.

IGST (Integrated GST) stands for Integrated Goods and Services Tax. IGST is a tax imposed on all interstate supplies of goods and services between two or more states/Union Territories. It is governed by the IGST Act 2017.

Under intrastate transactions, CGST and SGST are both applied. At the same time, IGST combines these into a single tax for goods and services moving between states or union territories. The tax is then shared between the central and state governments.

UTGST (Union Territory GST) is a tax imposed on the supply of goods and services within Union territories whose governments don’t have their own legislature. It is governed as per the UTGST Act 2017. It applies to the following Union territories:

- Ladakh

- Andaman and Nicobar Islands

- Chandigarh

- Dadra & Nagar Haveli

- Daman & Diu

- Lakshadweep

Union territories of Delhi, Jammu & Kashmir, and Puducherry have their own legislation. Hence, SGST taxation law is applicable here and not UTGST.

GST RETURN FILING

• Outward supplies (sales)

• Inward supplies (purchases)

• Input Tax Credit (ITC)

• Tax payable, paid and refund claimed

Returns are filed electronically on the GST Common Portal as per Sections 37 to 48 of the CGST Act, 2017.

TYPES OF GST RETURNS

| S. No. | Return | Purpose | Filed By | Frequency | Contains | Use |

|---|---|---|---|---|---|---|

| 1 | GSTR-1 | Outward supplies (sales) details | Regular taxpayers | Monthly / Quarterly | Invoice-wise sales, Debit/Credit notes | — |

| 2 | GSTR-2A | Purchase details (auto-generated) | Not filed by taxpayer | Auto | Supplier GSTR-1 data | ITC reconciliation |

| 3 | GSTR-2B | Static ITC statement | Not filed by taxpayer | Monthly | Eligible & ineligible ITC | For GSTR-3B |

| 4 | GSTR-3B | Summary return & tax payment | Regular taxpayers | Monthly / Quarterly | Sales, ITC claimed, Tax paid | — |

| 5 | GSTR-4 | Composition scheme return | Composition taxpayers | Annually | Turnover & tax at fixed rate | — |

| 6 | GSTR-5 | Non-resident taxable return | Non-resident taxpayers | Monthly | Taxable supplies | — |

| 7 | GSTR-6 | ISD return | ISD registered entities | Monthly | ITC distribution details | — |

| 8 | GSTR-7 | TDS under GST | TDS deductors | Monthly | TDS deducted & paid | — |

| 9 | GSTR-8 | TCS by e-commerce operator | E-commerce operators | Monthly | TCS collected | — |

| 10 | GSTR-9 | Annual return | Regular taxpayers | Annually | Annual sales, purchases & tax | — |

| 11 | GSTR-9A | Composition annual return | Composition taxpayers | Annually | Annual summary | — |

| 12 | GSTR-9C | GST audit reconciliation | Specified turnover taxpayers | As applicable | GST vs audited accounts | — |

| 13 | GSTR-10 | Final return | Cancelled GST holders | One-time | Closing GST details | — |

| 14 | GSTR-11 | UIN holder return | Embassies / UN bodies | As applicable | GST refund claims | — |

GST RETURN DUE DATES

For Regular Taxpayers

| Return | Purpose | Frequency | Due Date |

|---|---|---|---|

| GSTR-1 | Sales details | Monthly | 11th of next month |

| GSTR-1 | Sales details | Quarterly (QRMP) | 13th of month after quarter |

| GSTR-3B | Summary & tax payment | Monthly | 20th of next month |

| GSTR-3B | Summary & tax payment | Quarterly (QRMP) | 22nd / 24th (state-wise) |

| GSTR-9 | Annual return | Annually | 31st December of next FY |

| GSTR-9C | Audit reconciliation | Annually | 31st December (if applicable) |

For Composition Taxpayers

| Return | Purpose | Frequency | Due Date |

|---|---|---|---|

| CMP-08 | Tax payment statement | Quarterly | 18th of month after quarter |

| GSTR-4 | Annual return | Annually | 30th April of next FY |

REGULAR VS COMPOSITION SCHEME

| Basis | Regular Scheme | Composition Scheme |

|---|---|---|

| Tax Rates | Normal GST rates (0%, 5%, 18%, 40%) | Fixed low rate (1% / 5% / 6%) |

| ITC Claim | Allowed | Not allowed |

| GST on Invoice | Shown separately | Not shown |

| Interstate Sales | Allowed | Not allowed |

| Return Filing | Monthly / Quarterly | Mostly Annual |

| Compliance | High | Low |

| Suitable for | Medium & Large Businesses | Small Businesses |

| Annual Turnover Limit | No limit | Up to ₹1.5 crore (₹75 lakh for special states) |

FREQUENTLY ASKED QUESTIONS (FAQs)

The GST registration threshold is ₹20 lakh for service providers and ₹40 lakh for goods suppliers. For special category states, the limit is ₹10 lakh.