Ensure Compliance

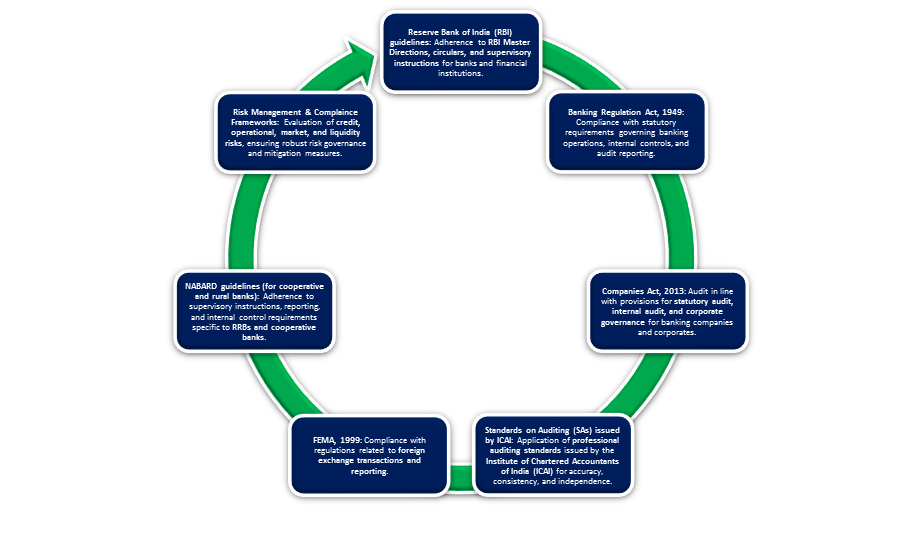

Verify adherence to statutory laws, RBI guidelines, Companies Act provisions, and internal policies.

Strengthen Internal Controls

Assess the effectiveness of financial, operational, and IT control systems..

Risk Identification and Mitigation

Identify credit, operational, market, and liquidity risks and recommend mitigation measures.

Enhance Operational Efficiency

Evaluate processes to improve productivity, efficiency, and resource utilization.

Detect and Prevent Fraud

Identify weaknesses and irregularities to prevent errors and fraudulent activities.

Support Management Decisions

Provide actionable insights and recommendations to aid strategic and operational decisions.

Promote Transparency and Accountability

Facilitate clear reporting and governance for boards, management, and stakeholders.

Safeguard Assets

Ensure protection of organizational resources, cash, and investments.

Facilitate Regulatory Oversight

Support effective supervision by regulators and compliance reporting.

Build Stakeholder Confidence

Strengthen trust among investors, regulators, and internal stakeholders through independent assurance.